I don’t quite know when it happened, or just quite how it happened, but a long time ago in a galaxy far far away ‘Investment’ & ‘Property’ got together and hatched a sinister plot… a plot to overthrow all other types of investments and become the power couple of the investment universe. Bonds got pushed aside, Alternative Assets were relegated to another realm, and shares were muscled out of their rightful place by Investment’s side. The new power couple launched a propaganda campaign, and convinced the Australian public that they were the rightful rulers of the investment universe. The campaign spread and was passed through the generations – ‘properties are investments / investments are properties’….but only a few resisted and questioned the source of the Investment / Property alliance’s power – one of the most powerful & evil forces in the investment universe. CHEAP DEBT.

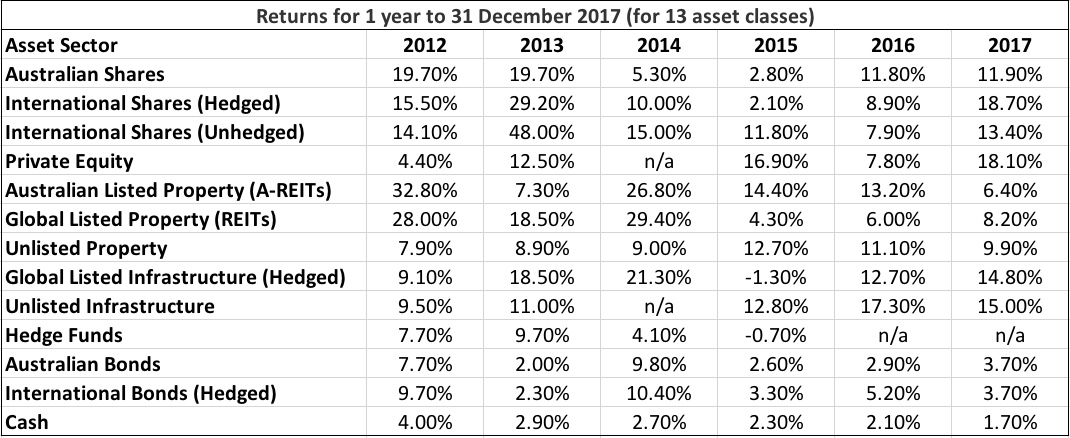

Well, what i’m talking about is the fact that in Australia, in a fair fight, from 2012 to 2017, shares beat unlisted property on 4 out of 6 years… but no one ever seems to talk about investing in a share portfolio.

But, unfortunately it wasn’t a fair fight. Property was propelled along by the use of cheap debt (leverage), and investors were able to make some spectacular returns. How does this work? If we oversimplify and assume property has no running costs, or entry & exit costs it looks something like this.

| A | Purchase Price | $400,000 |

| B | Deposit (your hard earned) | $80,000 |

| C | Value after 5 years | $700,000 |

| D | Profit | $300,000 |

| D/A | Return on Assets | 75% |

| D/B | Return on Investment | 375% |

In reality though, property investors have to service debt for 5 years, pay stamp duty, rates, water, maintenance, realestate management fees, conveyancing, selling costs (more conveyancing, sales commissions etc), so our real profits would have been reduced by the difference in rent received and these costs (after factoring in any tax benefits or liabilities).

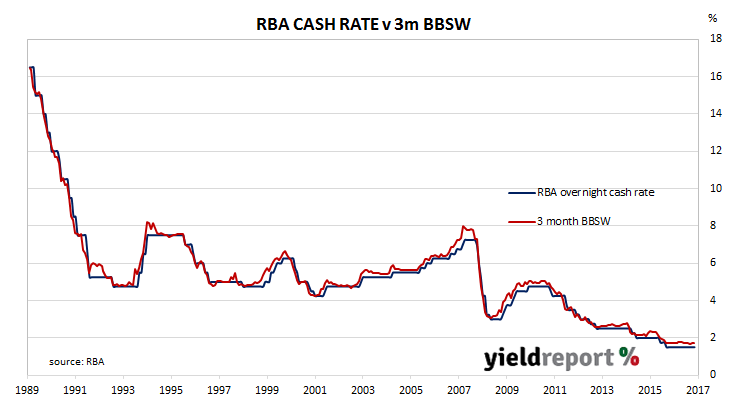

And what has happened over the last 20 years to investors ability to use leverage? Interest rates have fallen from >16% in 1989 to <2% in 2018. To put that in perspective – if the cost of debt was 16% in 1989, borrowing $100,000 cost you $16,000 in interest per year. Today, at interest rates of 4%, your $16,000 in interest would service a debt pile of $400,000 – that kind of cheap debt gives you a hell of a lot of purchasing power… but it also pushes asset prices through the roof! If houses become more and more affordable because investors can borrow more and more, demand increases, and prices rise – Its simple economics. The flip side of course is that now we have the lowest interest rates in history, and the longest run of no interest rate changes, rates will inevitable rise. leverage will become harder and harder to get, and the playing field may be levelled a little more.

So with that little back story, hopefully you can see why property has becoming such a popular investment – but its important to remember that its not the only game in town. I love my property as a wealth building asset class, but i also love shares (being a part owner in some of the worlds most exciting and profitable businesses). A combination of both of these high growth asset classes can be a very powerful way to build wealth for the long term so lets look at the pros and cons.

*Note that the term ‘property’ when used by investment professionals includes ALL property, from residential to office buildings, and industrial developments. When used by most members of the general public, they are referring to residential property. For more info, on all types and investing in all of them, check out 8 ways you can invest in realeastate.

Property:

Pros:

- Easy use of leverage (ability to borrow) – though getting harder with recent changes in lending rules.

- Its tangible (you can touch it and feel it and that provides comfort & security for some people)

- Opportunity for Capital Gains & Income

- Tax benefits (though some benefits such as depreciation and travel have been curtailed in recent changes in legislation)

- “Markets within Markets” – different regions perform differently at different times.

- Lack of Liquidity (being harder and more expensive to buy & sell forces you to hold for long periods – which is the whole point of investing, as opposed to trading)

Cons:

- High entry /exit costs – at a 90% LVR, even a modest $300,00 house costs you $30,000 + stamp duty, and on costs.

- High ongoing costs – Management fees, insurance, rates, water, and maintenance can easily reduce a gross rental yield of 5% down to a net yield of 3.5%

- The flip-side of leverage is when prices go down, your losses can be amplified – 10 fold for a 90% loan to value ratio!

- Banks own the property until you pay it off. If you end up with negative equity, then can demand you increase your equity.

- Low liquidity – buying and selling houses is kind of a big deal so its not easy to turn property into cash and vice versa.

- Lack of diversification – because they require such a large chunk of cash, your first foray into property probably means you’re massively overexposed to this asset class.

- Your purchasing power (ability to invest in the next asset) is capped by your serviceability. If you reach your max debt position, thats it, your done. You have to put your property acquisition plans on hold, sell something, or get a pay increase.

Shares:

Shares are often passed off as risky, volatile, gambling, or some kind of sheer luck investment class. This couldn’t be more incorrect. Over the long-term, shares and property have had very similar investment returns (despite the more pronounced hiccups along the way with shares). The sheer fact of the matter is that investing in the sharemarket is grossly misunderstood – but everyone understands renting out a house.

A share is a part ownership in a business. A share entitles you to vote on the election (or sacking) of the businesses directors, and on important company resolutions. It entitles you to part of the profits of the business, and it allows you to partake in its growth. Who wouldn’t want a part of the biggest and best companies in the world. Imagine being a part owner of Apple, or Google, or Netflix, or Paypal, or Microsoft, or Alibaba… These beasts have transformed our lives – and they may insane profits – *and my wife is a part owner of all of them via her investment in one Listed Investment Company (LIC).

*Not quite a true owner in this case, because the LIC has direct ownership of the companies, she just owns shares in the LIC. (as opposed to buying shares in each of the companies directly)

Pros:

- High growth asset class

- High liquidity & cheap entry / exit costs

- buying or selling up to $10,000 of shares can cost you $19.95 through the major online brokers (or even less through others)

- A purchase or sale is settled within 48 hours – cash & shares (or managed fund) can be interchanged very quickly.

- Easy access to professional investment managers via Managed Funds, ETF’s, LIC’s, or LIT’s.

- You can still use leverage in exactly the same way as property (albeit at slightly lower LVR’s)

- You can invest internationally with ease

- You can invest in companies who invest in types of property that are usually inaccessible to individual investors. (office blocks, warehouses, or shopping centres for example)

- Invest in different market sectors (IT & Tech, Mining, Healthcare, Retail, or whatever else takes your fancy)

- Benefit from a combination of growth & income from dividends (in a combination that suits your requirements)

- Tax benefits from franking credits

- Maximum diversity – investing even $2000 in a managed fund could gain you exposure to multiple countries, multiple industries, and hundred of companies.

- Unmatched transparency & ability to track the progress of your underlying investments -Access to company financial statements twice yearly (or quarterly for USA companies)

Cons:

- Higher volatility

- High liquidity (tempting people to buy / sell too frequently)

- Higher learning curve than simple property investing (which is why using managed funds is a good place to start!)

- Direct share investing can be risky for novice investors.

- Can be influenced in the short-term by macro-economic events

- Building a well diversified direct share portfolio probably requires a minimum of 20 companies – which increases the amount of investment capital required, or increases risk if you scale back the number. (Which is why managed funds are such a good option)

- Companies can go bankrupt and the value of your shares could fall to 0. Again, this is why diversification is important, and why using a fund manager makes sense.

So, are shares or property the best investment?

Dammit, why do we always have to have this argument? Holden vs Ford, Rugby League vs Rugby Union, Snowboarding vs Skiing?… can’t we all just get along?

The reality is that shares and property have performed differently at different periods – and that makes them the perfect partners in a diversified investment portfolio. There is no need to choose – you can have your cake and eat it too…

A diversified investment portfolio gains you exposure to all asset classes; International Shares, Australian Shares, Property, Infrastructure, Bonds, Cash, Debt & Alternatives – and we can resize, or tailor the slices of pie to suit an individuals personal circumstances. Maybe more property is right for some, may more shares is right for others. The exact mix is a complicated consideration of all of your various life circumstances, needs and wants – but getting it right means you’ve got the best risk / reward tradeoff, and the best chance at meeting your target investment returns.

If you’re thinking about investing in property or shares, get in touch for a chat. It may just kick start your enthusiasm for investing, help you on your investing journey, or help you avoid some of the early investing mistakes that are all too common, but easily avoidable.

All the best.

Saul.